Abstract

Have you ever wondered, if we do not add the right pinch of salt to a burger, will it taste good? The answer is no. If the burger ingredients are not in the right mix, the burger will not taste good. Similarly, to create a valuable crypto asset we need to have the right mix of tokenomics. Tokenomics is the recipe to create valuable crypto assets. In a world where thousands of crypto assets exist, tokenomics help us read between the lines and show us the path to make sound investment decisions.

In this issue of The Bridge, we present the main ingredients that make up for a good tokenomics. We find four key ingredients. They are (i) the total supply and its demand, (ii) the initial allocation of tokens, (iii) the distribution of tokens and (iv) the value accrual. Before we present the ingredients in detail, let us start with the beginning; what is tokenomics?

What is Tokenomics?

Tokenomics is the rulebook defining a crypto asset1 monetary policy, from the issuance to the removal of tokens, if any. It uses game theory to design incentives to reward good actors and punish bad ones. Tokenomics also defines the role that the token plays in the ecosystem and how it accrues value.

Tokenomics are necessary because public blockchains are open to everyone, including bad actors. Tokenomics align the behaviour of each actor, strengthen the protocol and create trust ultimately. It does it with the help of crypto assets. An increase in good behaviour materialises in a rise in the value of a crypto asset, which encourages participants to be good actors.

Harvard psychologist, B.F. Skinner first proposed the idea of Tokenomics in 1972. He believed a token economic model could be beneficial to align behaviours.

In well-designed tokenomics, all costs and benefits are internalised (no externalities) so that there is no way to game the ecosystem, making it robust.

Four different actors participate in all blockchain projects. They are the founders and the developers who build the project, the miners or validators that run the blockchain and provide security, the investors who provide the capital required to make the project and finally, the consumers as the ultimate users of the platform. Tokenomics creates a set of rules aligning all the actors and reinforcing the ecosystem.

Total supply and its demand

The first key ingredient in tokenomics is the token supply, whether it is capped or unlimited, and the demand to complement such a supply. Bitcoin is well known for having a capped supply of 21 million bitcoins while Ether supply is unlimited. It is interesting to note that the two most successful blockchains measured by market capitalisation have different monetary policies.

Both are successful because the services they offer are different, and their token policy reflects these differences. Bitcoin is perceived as digital gold, a scarce resource whose issuance schedule is known in advance. As the demand for bitcoin has been ever-increasing and the supply is capped, the price of bitcoin has increased significantly.

Ethereum has a different use case. It is a general-purpose blockchain designed to support many applications, like the famous decentralised applications (dapps). Ether’s (ETH) primary role is to pay for computation fees to the system to process the transaction. In that sense, ether is mainly a medium of exchange – while bitcoin is a store of value – and an unlimited money supply is appropriate owing to the ever-increasing uses and dapps being built on top of Ethereum.

br>In both cases, coin issuance follows strict and hard-coded rules defined by the tokenomics. Whether capped or unlimited, the token policies are disciplined and a source of trust.

The other side to note is the demand for a token. Token demand may be generated through the utility it provides or the rights it grants to the token owner. Some tokens are utility based that have a use within the ecosystem, such as LINK. For every request that is made of Chainlink’s oracle services, the price is paid in LINK. UNI has no utility but the token holders get a vote in the protocol’s governance, including control over its multi-billion-dollar treasury. Token holders may also accrue all or a part of protocol revenue directly or indirectly. For example, the treasury income of Yearn Finance is used to buy back YFI from the open market, indirectly benefiting token holders. SushiSwap stakers earn five basis points on all trades if they stake their SUSHI tokens on the platform.

Proof-of-work blockchains like Bitcoin and Ethereum are also utility tokens as they are used to pay for the transaction fees on the networks. Proof-of-stake tokens like Polkadot and Cardano are both utility and governance tokens. Along with paying for transaction fees, stakers also vote on the future direction of the protocol.

Bitcoin and Ethereum successes result from the match between supply characteristics and the demand for the services.

The right match between use case induced crypto-asset demand and token supply incentivise miners and validators to add security to the blockchain as they are attractively rewarded for the tasks they perform. In addition, users find the currency attractive as an investment and pay a fair price for the service used or rights granted. All these reinforce the attractiveness of the blockchain and the ecosystem.

Initial allocation of tokens

A blockchain project needs time and resources to go live. To attract early investors, developers and other talents, tokens are often allocated in advance to this group. If the project goes live and the value of tokens increases, they get rewarded for their effort.

The initial allocation of tokens among this group is an essential element for a project’s success. The percentage needs to be significant enough to motivate the contributors but not too big to challenge the fundamental idea of decentralisation.

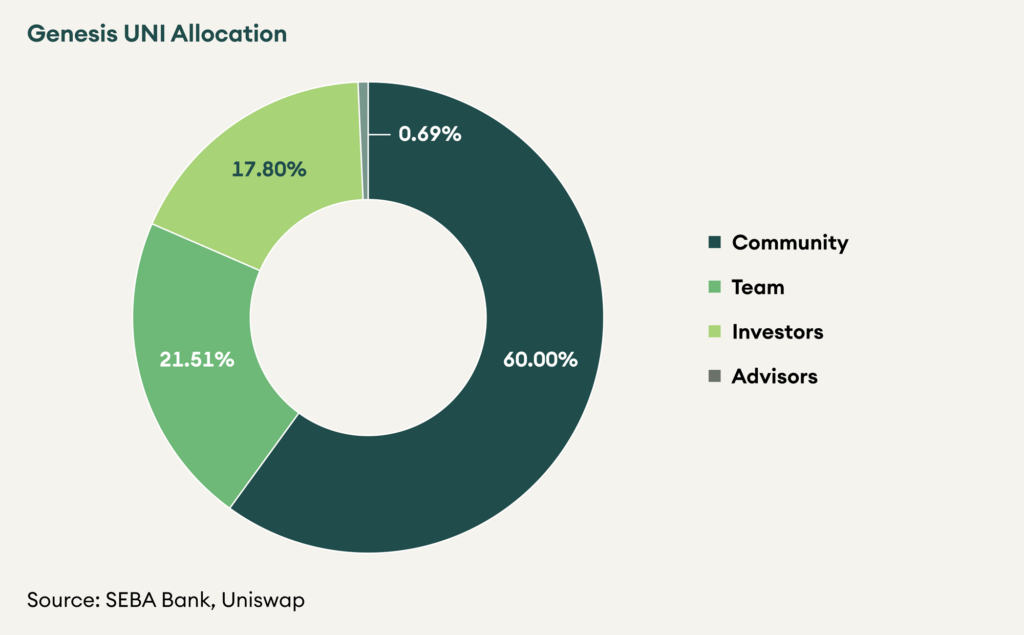

The example below shows the initial token allocation for Uniswap protocol, UNI, a decentralised exchange to swap Ethereum-based crypto assets. As we can see, the allocation of tokens is complex and include several stakeholders. The challenge is to propose an allocation that pleases all participants.

Figure 1: UNI token allocation

Notice that tokens allocated at an early stage are often subject to a vesting period. This is another incentive for early participants to continue supporting the projects in the initial years of its life until it creates a sustainable ecosystem of its own. The vesting period applies predominantly to pre-mined crypto assets, i.e. crypto-assets issued before the project goes live.

Fully diluted2 market value and token unlocks are an important thing to watch when one is about to invest in a token because a massive unlock can dilute one’s holdings. While a predefined token allocation like Uniswap is common as more and more blockchain projects are run similar to start-ups, there also exist projects where there is no team allocation.

Bitcoin (BTC) is emblematic of what is called a fair launch. In a fair launch, tokens are distributed to the community from day one without reserving any tokens for developers and seed investors. Fair launch ensures that everyone has equal access to the distribution and should prevent the concentration of many tokens to any particular individual or entity at the token’s launch. It is transparent as everyone gets access to tokens or coins based on criteria other than a public sale.

Yearn Finance (YFI) was also a fair launch. All tokens were distributed initially to stakers with no reserves for the founder or the protocol. However, after the initial distribution, it found it difficult to attract talented strategists and developers with no treasury reserves and eventually mint new tokens to incentivise the development team and strategists.

A fair launch worked well to make bitcoin the most decentralised project and asset in history, but for a dapp like Yearn Finance under continuous development, some treasury reserves are required to ensure proper alignment of incentives.

Distribution of tokens

Once the allocation is decided, the distribution of tokens may start. We differentiate this between two episodes, the genesis block and the following ones.

The genesis block is the first block of a blockchain and plays a particular role. It makes the initial distribution of tokens and must make it so that the blockchain becomes operable. This means that all ecosystem participants need to get tokens to create an economy and start it. The participants are the miners, the validators that provide the security and the users. To take an analogy, the genesis block is when Monopoly players receive their first allocation of notes to start the game.

In the subsequent blocks, token inflation starts. While inflation sounds negative, it is a way to reward active participants and distribute further tokens in the economy. As the economy grows with the number of actors and transactions, the tokens must follow suit to maintain a delicate balance between circulating supply and demand.

For layer-1 crypto assets, the increase in token supply, the inflation, is distributed to miners and validators for each block proposed; this is called block rewards. In the case of bitcoin, the block reward is currently 6.25 BTC and halves every four years. By rewarding these crucial actors, tokenomics incentivises them to act honestly, create trust, and ultimately increase the crypto asset’s value. The more valuable the tokens, the more incentivised are miners and validators, reinforcing the blockchain. As in the real economy, money inflation does not harm as long as it is proportionate to economic growth.

While bitcoin uses a Proof-of-Work (PoW) algorithm, other blockchains such as Polkadot uses a Proof-of-Stake (PoS) one. In PoS, tokens holders are incentivised to stake their coins to get a yield, which is usually higher than the inflation schedule. As a result, staking coins protect against the dilution caused by inflation. It also helps you accumulate more coins over time and add security and trust in the system, creating a win-win situation for the coin and the coin holder.

Early inflation is often high as the goal is to encourage early adopters to use a new blockchain. In the case of Bitcoin, the block reward started at 50 BTC.

In the last two years, we have observed the creation of new services based on existing blockchains. For instance, Decentralised Finance (DeFi) applications such as Uniswap are built mainly on top of Layer-1 solutions like Ethereum. As the underlying network provides the security of these applications, the issuance of DeFi tokens, for instance, incentivise other behaviour. Early adopters of DeFi protocols provide liquidity to these financial applications and are rewarded for that. This is called liquidity mining. Again, the earlier liquidity is provided, the higher the annual percentage yield (APY).

In the Polkadot ecosystem, blockchains (called parachains) are attached to the relay chain (the Polkadot chain) to benefit from its security. To do that, DOTs are bound, and parachains issue their own currencies to reward early adopters via an auction process.

Value accrual

The last essential ingredient of tokenomics covers the value accrual of a token.

Value accrual is when the usage of a blockchain or a dapp confers some value to the token and benefits the investors. This relationship is not always direct and the mechanism by which value accrues plays a large part in how favourable the market views the token and its price.

For layer-1 PoW protocols, as described earlier, the tokens are usually utility tokens that are used to pay for the transaction fees. Bitcoin receives a premium for being a store-of-value and being a permissionless system to exchange value. It has built this narrative as the oldest and most decentralised blockchain with a solid monetary policy and proven censorship resistance.

PoS protocols accrue value by securing the network and earning validator rewards and transaction fees in return. They also get a governance vote which decides the direction of the protocol. This control is valuable, and value is accrued as the protocol increases in significance.

As far as dapps are concerned, it is worth noting that smart contracts can usually work perfectly fine even without a token. Therefore, the role a token plays in an ecosystem is crucial to understand.

Continuing the example of LINK, the question to ask is why Chainlink needs its own token to settle fees between a requestor of a data and the provider when it could be settled in ETH, USD or USDC? The reason it cannot be ETH is that since its inception, Chainlink has wanted to grow beyond a single blockchain, and it now provides oracle services on multiple blockchains like Polygon and Fantom, and it even seeks to further expand to other blockchains like Solana and Polkadot as well. A decentralised oracle cannot settle payment through wire transfers in USD, bringing an element of trust and asynchronous settlement. It cannot be a stablecoin like USDC or DAI, as they are also subject to either centralisation, or chances of protocol failure. As a result, an independent token was chosen to be the protocol currency for all participants. Node operators need to own LINK to run a node, and the requestor must make payments in LINK tokens. This is not exposed to any externalities and the protocol accrues value in line with Metcalfe’s Law. LINK exemplifies this relation well as its value has increased at the same time it has become ubiquitous throughout DeFi.

Similarly, Uniswap functioned perfectly fine with billions of dollar volumes even before its token launched in September 2020. UNI currently also does not earn any protocol fees from the swaps carried on the protocol. However, UNI is a governance token, it confers significant control over the protocol. Holders have the right to spend its multi-billion-dollar treasury and update the protocol, for example, collecting fees from trades.

Some projects also create deflationary trends to reduce the supply of coins from the market by buying back the coins in circulation from its earned revenues. This process is called “burning” and is comparable to a stock buyback. The aim is to reduce the circulating supply to boost the token’s price. YFI, ETH and BNB are deflationary coins that use part of their earnings to buy back the token from the open market.

Conclusion

Tokenomics plays a central role in the functioning of a blockchain or dapp. It uses a set of hard-coded rules and a token to align the behaviour of all actors in a way that benefits the protocol. As we have seen, there is not one good tokenomics model. There are several recipes for good burgers with different ingredients leading to various flavours. For each recipe, the right mix of ingredients is key. Depending on the blockchain services offered, tokenomics are different.

Four ingredients are essential. The first one is the total supply and demand. The number of tokens in circulation must fit the token demand. The second element is the initial allocation of the token. It must incentivise all participants to the network without harming anyone. The third component is subsequent token distribution. It has to be made dynamically and reward participants correctly without diluting the value of the ecosystem. Finally, value accrual gives the token value and cement its place in the ecosystem.

1In this publication, we use the words crypto asset, token and coin indifferently. ↵

2Fully diluted market value is the market capitalisation if all the tokens were issued. In the base of Bitcoin, this would be the market capitalisation at current price and with 21 million bitcoins. ↵