Abstract

Polkadot is a promising project that should interest investors. First, interoperability increases digital asset utilisation, and Polkadot offers all the broadest type of interoperability. The success of DeFi, as a specific interoperability application, shows the potential of these types of solutions. Second, Polkadot and its framework Substrate democratise blockchain development. We expect developers to use this platform to populate the ecosystem with new applications. Both these points together are likely to help Polkadot achieve higher network effect.

Introduction

In the November 2020 Digital Investor, we introduced blockchain interoperability or blockchains’ ability to exchange information between different ecosystems. We concluded that interoperability facilitates secure and trustless value exchange, and we expect interoperability solutions to capture value in the future. Therefore, we think that interoperability solutions demand investor attention.

Interoperability may take many forms. In this edition of the Digital Investor, we focus on interoperability in a broad sense. Polkadot aims to connect all types of blockchains and transfer all types of messages between them. We briefly present the project in terms of its architecture, consensus mechanism, and stakeholders before analysing the economics and estimating its investment attractiveness.

The foundation of Web 3.0

Polkadot is a “layer 0” solution to connect all blockchains and enable cross-blockchain transfers of any data and asset, not just tokens. It aims to be the foundation of Web 3.0 as per Gavin Wood, the creator of Polkadot and co-founder of Ethereum.

A layer 0 solution is a protocol that lays below level 1 solutions such as Bitcoin, Ethereum and other altcoins blockchains. It is there to make them communicate, interact, in one word to make them interoperable. Ultimately, interoperability allows to weave links between the chains and form a web of a new type: web 3.0. This technology gives “the user strong and verifiable guarantees about the information they are receiving, what information they are giving away, and what they are paying and what they are receiving in return.“1

Polkadot offers economic scalability by enabling a common set of validators to secure multiple blockchains (shared security). Polkadot is to blockchains what Ethereum is to smart contract applications: a platform. With this parallel in mind, Polkadot is a layer 0 solution on which layer 1 chains are deployed, and Ethereum is a layer 1 solution on which layer 2 smart contracts run. Each layer benefits from the security of the lower layer.

Polkadot provides a web application called Substrate to “create custom blockchain in minutes”. With this developer-friendly framework, Polkadot provides a multi-language software with build-in function to facilitate blockchains’ creation.

Architecture

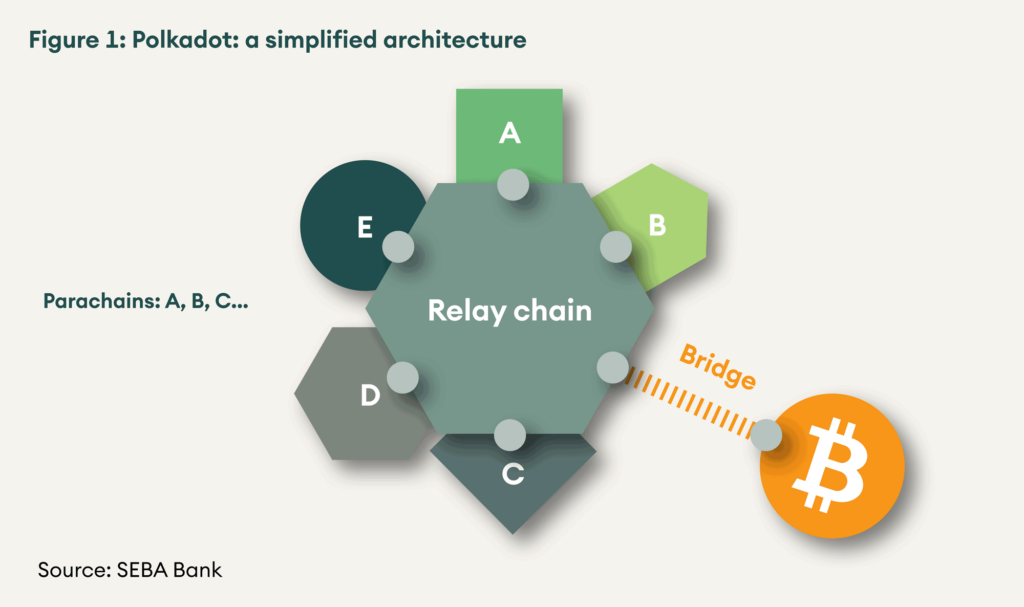

The Polkadot blockchain network revolves around the general relay chain/sidechain architecture, as illustrated in figure 1. At the centre of the ecosystem is the relay chain – the Polkadot blockchain – surrounded by sidechains, called parachains2 in the Polkadot ecosystem. Parachains can be built with Substrate, which allows them to connect automatically with the relay chain. For non-parachains (e.g. Ethereum, Bitcoin) bridges3 are needed to connect.

Consensus mechanism

Polkadot has developed its own of Proof-of-Stake consensus mechanism variation called NPoS or Nominated Proof-of-Stake. In addition to providing security, a key feature of NPoS is to promote decentralisation. There are two ways to promote decentralisation.

Firstly, validators need to put capital at risk to propose blocks. To accommodate more validators, protocol allows nominators to nominate validators and back them with capital. It incentivises nominators by rewarding them a share in validators’ income. They can nominate up to 16 validators. Another feature designed to increase decentralisation is that the validators’ rewards are not proportional to the amount at stake. All validators selected to participate in an era – a time slot of 24 hours – receive the same compensation at the end. In other words, validators are encouraged to have enough total (validators and nominators) capital at stake but not too much as the reward is not proportional to it. According to this logic, all validating nodes must have the same capital at stake at equilibrium to maximise their return on investment. (For a good introduction to NPoS, click here).

Without going into the details, it is worth mentioning that Polkadot splits the protocol consensus mechanism into two parts to allow all types of parachains and non-parachains to share data efficiently. Block production is governed by BABE (Blind Assignment for Blockchain Extension), an engine that offers liveliness and probabilistic finality. As Probabilistic finality is not enough for interoperability, a finality gadget named GRANDPA (GHOST-based Recursive Ancestor Deriving Prefix Agreement) finalises the blockchains, not the blocks, as it decides on the canonical chain.

Because of this split consensus mechanism, to change the history of a parachain implies rewriting the entire history of the relay chain. As such, the security of each parachain is delegated to the relay chain and the security is shared.

Stakeholders

The functioning of the relay chain/parachain architecture sketched above relies on four participants: the validators, the nominators, the collators and the fishermen.

The validators are full-node relay chain performing the usual validating tasks of a Proof-of-stake (PoS) consensus mechanism. They propose blocks to the relay chain, build the network security and get rewards from staking, fees, and tips. Notice that validators interact with collators – to be explained later – but do not need to participate in parachains as full-nodes.

The nominators are stakeholders who back and select validators. This can be done from a light client, and they do not need to have any awareness of parachains. By putting Polkadot’s native currency (DOT) at stake, they delegate security to validators and get part of the validators’ rewards in return.

The collators are full-node parachains collecting parachains data and transferring it to validators. They are chosen by parachains stakeholders but do not participate in the relay chain consensus mechanism and do not stake DOT. The way collators are rewarded is not defined in the Polkadot protocol; each parachains decides how to do it.

The fishermen are bounty hunters performing additional security checks on the correct operation of the parachains and relay chain, on behalf of the relay chain which supplies the reward. They get rewarded when they find a compromised block. The block’s creator receives slashed (up to 100% of its total stake, i.e. validators and nominator stake combined) and the fishermen receive a fraction of the stake. Notice that fishermen also stake DOT to prevent Sybil attacks from wasting ‘validators’ time.

Economics

Polkadot economics is organised around its native currency. DOT fulfils primarily three functions in the ecosystem. It provides network security when staked by validators and nominators, it offers governance right to its holders, allowing connecting parachains when bonded.

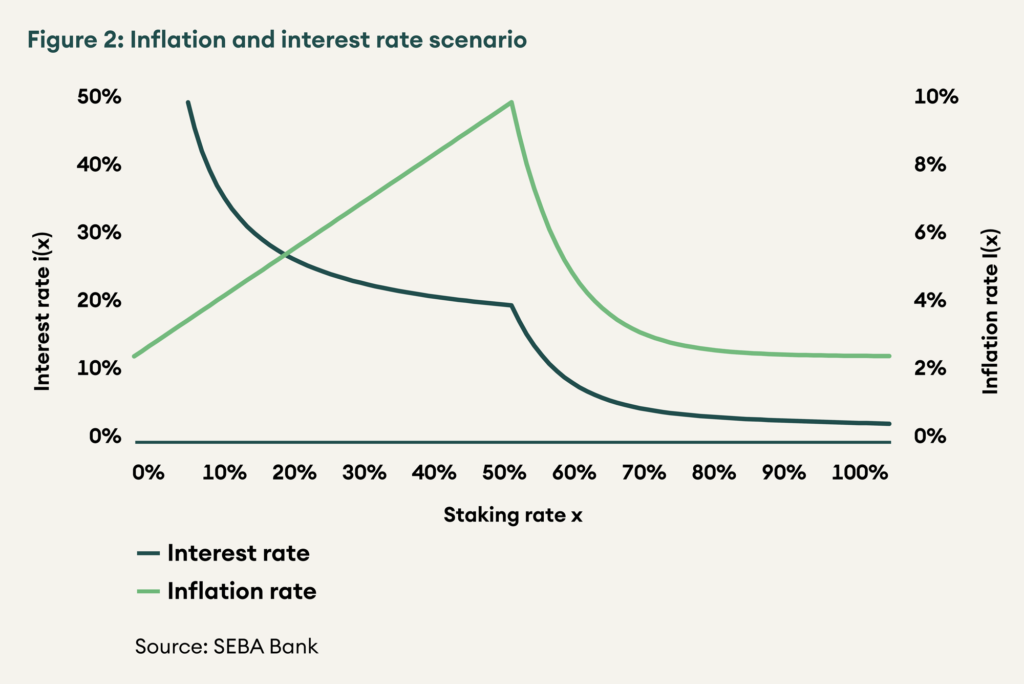

At the ecosystem level, the DOT monetary policy is rule-based. The inflation reaction function depends on the staking ratio and the interest rate received by stakers (validators and nominators):

Where x is the staking ratio, I(x) is the inflation rate, i(x) the annual interest rate.

The staking ratio is the proportion of DOTs staked relative to the total number of DOT in circulation. According to the current rule, the ideal staking ratio (in an ecosystem with parachains) is set at 50%, and the interest rate at ideal staking is 20%, leading to a 10% inflation rate4.

Looking at the inflation function, we see that inflation varies between a minimum of about 2.5% and a maximum of 10% achieved at the ideal staking rate (see figure 2). The farther the staking rate is from its ideal value, the lower the inflation rate. Notice that the function is asymmetric. Inflation increases linearly with the staking rate when the latter is smaller than its ideal value and decreases suddenly if the staking rate is too high.

With this asymmetry, the interest rate perceived by the stakers declines progressively until the ideal staking ratio is achieved and declines massively thereafter. As a result, if the network security would be at risk due to insufficient staking, the suddenly high-interest rate incentivises new stakers to join. The other way round, when staking is sufficient (above the ideal staking ratio) market forces define the equilibrium ratio as stakers arbitrate between different staking options.

In comparison to other staking algorithms, an ideal staking ratio of 50% is low. Cosmos, another interoperability solution targets 67%, for instance. The low ratio results from the parachains auction mechanism that consists of bounded DOT, which is expected to represent about 30% of all available DOT5. Whith this in mind, about 80% of all DOTs would be illiquid and participating in security.

No parachains auction has taken place so far. The first auction should take place this quarter. For a parachain to connect to the relay chain, DOT needs to be bonded. Contrary to staked DOT, bonded DOT do not receive any rewards as defined by the protocol. The rationale behind the absence of rewards is that parachains need to pay for the relay chain services: interoperability and shared security. The price to pay is inflation dilution. Inflation dilution is the trade-off parachains have to make for the benefits.

Notice that the Polkadot protocol does not rule parachains economics; each parachain is free to design its functioning. How DOTs are accumulated to participate in auctions and how collators are remunerated depend entirely on parachain governance.

Users and speculators hold the remaining 20% of DOTs. To use the network, users will need to pay fees to validators. Fees vary according to the size of the message and utilisation. Again, a rule is there to smooth the fee cycle and to avoid destabilising spikes in case of congestion.

Congestion is unlikely to happen soon nonetheless. In an ecosystem with 100 parachains, the number of transactions could theoretically reach 1 million transactions per second (TPS). More realistically, real-world simulations indicate that 80,000 TPS is feasible. In comparison, Ethereum 1.0 offers about 15 TPS and Ethereum 2.0 is expected to provide 100,000.

Valuation

Valuing native digital assets is challenging as there is no universal model available to estimate a token’s dollar value. To help investors evaluate a blockchain project’s solidity and attractiveness, we have developed a comprehensive investment framework we apply here.

The Polkadot investment thesis is to be the foundational layer of Web 3.0, a new iteration of the internet where users own their data and values can be transferred without intermediaries between chains (interoperability). To achieve this goal, Polkadot offers a unique feature: shared security. It is set to encourage new parachains – chains built on Substrate – to populate the ecosystem and benefit from the entire network’s security from day one. In many ways, public blockchain’s security is a function of how strong the community is. Creating a vibrant community from scratch is an uphill task. Polkadot offers new projects much needed security so that their teams can focus on building applications.

The Polkadot development team has developed a new protocol that offers security (economics), decentralisation (1000 validators) and scalability (80’000 TPS). While the chain is live, and even though there is no parachain currently, there is good reason to believe that the protocol is reliable. Kusama, the unaudited version of Polkadot (Polkadot ‘Canary’s network), is running smoothly.

The NPoS consensus algorithm is also new. In comparison to DPoS where the risk of staking concentration is elevated, NPoS distributes staking reward evenly among stakers, leading to a better distribution of tokens and thus more decentralised network.

The token economics looks solid as the incentives are designed to attract stakers to provide security. The fee structure coupled with the project’s high scalability should smooth out spikes in fees and make transactions affordable for users while simultaneously remaining rewarding for stakers.

Some questions remain open nonetheless. For instance, the underlying game-theoretical model has not been solved and is not clear whether it has one or multiple equilibria. In Game Theory, an equilibrium is a solution to a game. If a game has several equilibria, there is a risk ending up in an undesired equilibrium.

Parachain auctions start this quarter. While the auction method is known, we don’t know how many DOTs will be bonded. This amount is crucial as it indicates the amount parachains are ready to pay to benefit from shared security. Finally, fishermen’s economics is weak because fishermen get paid if they catch someone misbehaving. As it is unlikely to happen too often, fishermen could be discouraged and forced to stop fishing, reducing the network’s security. One way to mitigate this issue is for validators to be fishermen as well.

The core team has outstanding experience in the public blockchain domain. It consists of Gavin Wood, Robert Habermeier and Peter Czaban, three experienced blockchain developers. The core team is strengthened by the Web3 Foundation and Parity technologies’ backing, two entities employing talented people.

According to the latest Electric Capital Developer Report, the number of developers active in any projects is growing fast. Developers who have been active for the first time in 2020 represent more than 40% of all developer communities. Looking at the most active projects measured by the number of developers, Polkadot is number three only after Ethereum and Bitcoin. Between Q3 2019 and Q3 2020, Polkadot doubled its developer count to 384. In terms of development history, Polkadot has attracted more developers for the same number of days since the first commit than Cosmos and Ethereum.

As mentioned earlier, Polkadot is live but not complete as there is no parachain connected. As a result, the network is still small. At the time of writing, the number of nodes is 550, with 266 active validators and 308 waiting to be added. A campaign to reach 1000 validators is in place. Though the number of validators is smaller than the other networks, the NPoS structure encourages decentralisation in two ways – keeping the same validator rewards regardless of their stake and allowing nominators to choose validators. As an illustration, more than 99% of staked DOTs belong to nominators, less than 1% belong to the validators. It suggests that ‘validators’ reputation plays a central role.

There are about 130 Substrate based projects in development, covering many topics such as Defi, wallets, identity solutions, social, smart contracts, file storage, IoT, Gaming, Bridge and infrastructure. According to this data, there is a strong interest in building chains with Substrate and connecting these native parachains to the relay through the auction process. As far as non-parachains are concerned, bridges for bitcoin and Ethereum should be rolled out in H1 2021.

Polkadot is equipped with on-chain governance. DOT gives the right to vote to its holders. The governanceis made of an elected council of 13 members that will gradually expand to 23. Besides it, there is a technical committee, not elected, but chosen by the Council. It represents the last line of defence and is responsible for fixing critical bugs. Except for it, the system is democratic. Proposals pass through a public referendum. An adaptive quorum biasing is used to avoid destabilising proposals to be accepted in case of low turnover. It consists of a supermajority to pass a proposal when the turnover is low and a simple majority when it is high. Notice that the Council manages a treasury whose aim is to fund proposals.

The financial situation of Polkadot is very healthy. After a bumpy start in 2017 marked by a hack, Polkadot raised close to $184 million in 9 rounds; the last one took place in July 2020 ($43.7 million). 30% of tokens (300 millions) were allocated to Web 3.0 foundation.

Polkadot is in direct competition with other interoperability solutions such as Cosmos and with Ethereum to some extent in terms of market share. In terms of market capitalisation, it is the biggest project among interoperability solutions. One of the main differences with Cosmos is that Polkadot provides shared security. Polkadot competes with Ethereum 2.0 to provide a scalable platform for smart contracts for the former and blockchains for the latter. Ethereum has a strong reputation, a large user base, high compossibility, and is the platform of choice for DeFi applications. It has just started a long journey, that will transform it into a scalable PoS blockchain. For Polkadot, there is a lot of uncertainty as the BABE/GRANDPA algorithm is untested, and it does not have any history so far. The key question to ask while allocating funds today between ETH and DOT is whether developers prefer building applications on the top of Ethereum or Polkadot to attract users. We think that both these blockchains will coexist in the future.

At the design level, Ethereum 2.0 and Polkadot are similar. Ethereum 2.0 has beacon chain to co-ordinate among different shards and provide security to all the shards. Relay chain is the beacon chain equivalent in Polkadot. While Ethereum’s shift to the new structure is a pivot from the old Proof of work chain, Polkadot has had the same design goals since the beginning and is probably ahead of Ethereum the end goal is concerned. Among all the projects, Polkadot is well-positioned to capitalise on any delays in Ethereum 2.0 roadmap. In short, we think that apart from the competition with Ethereum for project and developer share, Polkadot is also a put option on Ethereum 2.0.

Conclusion

Polkadot is a promising project that should interest investors. First, interoperability increases digital asset utilisation, and Polkadot offers all the broadest type of interoperability. The success of DeFi, as a specific interoperability application, shows the potential of these types of solutions. Second, Polkadot and its framework Substrate democratise blockchain development. We expect developers to use this platform to populate the ecosystem with new applications. Both these points together are likely to help Polkadot achieve higher network effect.

A special thanks to Bill Laboon, Fatemeh Shirazi, and Alistair Stewart for their explanations.

1https://medium.com/@gavofyork/why-we-need-web-3-0-5da4f2bf95ab ↵

2Parachains comes from parallel chains as they are running in parallel. The Polkadot architecture shares many similarities with Ethererum 2.0, where the beacon chain will, ultimately, becomes the relay chain, and the shards are the parachains. ↵

3Bridges are parachains whose goals are to connect non-parachains to the relay chain. ↵

4The equation presented here is simplified. In the white paper, this equation rule NPoS inflation, not total inflation as suggested here. The true relation being Inflation = Inflation NPoS + Inflation Treasury – Inflation slashing – inflation transaction fee. Also, for simplicity, the details of the inflation function are not presented, but the results are shown in figure 2. ↵

5The price for connecting a parachain may discourage some chains from connecting to the relay chain. For these chains, interoperability is possible with a pay-as-you-go system called parathread that consists of paying for every single inter-blockchain communication. ↵