Abstract

This new publication will shed light on cryptoassets as an emerging asset class and its fundamental drivers. We hope you will enjoy reading this publication and that you will find it helpful in understanding our investment scenarios.

Executive summary

Polarising forces are acting upon Bitcoin – on the positive side, we see El Salvador adopting it as legal tender, and Michael Saylor’s Microstrategy cannot seem to buy enough of it. But on the negative side, China is clamping down on the mining industry, and Elon Musk is greatly concerned about the environmental impact of mining. Against this backdrop, the price is hovering within a range, the hype cycle has cooled off, and user growth has slowed down after peaking in May 2021.

Other payment chains, Litecoin and Stellar, did not see a significant increase in price or user activity from their peaks in 2017-2018. These older generation chains find it challenging to attract new users for primarily two reasons. Their network, trustworthiness, and brand are smaller than the more established Bitcoin and Ethereum. Secondly, they cannot innovate as fast as the new protocols with new architecture and deep pockets.

Adoption in decentralised finance (DeFi) and non-fungible tokens (NFT) brought about new users to Ethereum, so much that it could not keep up with the demand, and gas prices became prohibitive. Consequently, it lost market share to other platform chains. With roll-ups around the corner, we expect to see Ethereum scale for the first time and look to regain its market dominance. An improvement in its tokenomics will also support Ethereum’s narrative.

Newer platform chains, Cardano and Polkadot are at a crucial juncture where the infrastructure is ready and prepared for the next leg of growth. Smart contracts will be going live for Cardano in Q3 2021, with DeFi and NFT applications to follow shortly after. Parachain auctions on Kusama are seeing good traction and Polkadot will be ready for its own once the auctions on Kusama conclude.

DeFi has seen a slowdown in the rate of growth in the past couple of quarters. However, its services are seeing being integrated by centralised crypto solutions. These seamless integrations will give DeFi protocols access to a new set of users.

Uniswap remains the top DeFi application, and participation by the community in its governance is growing. Yearn Finance sees an increase in deposits with users looking for passive yields as the trading environment is not as lucrative.

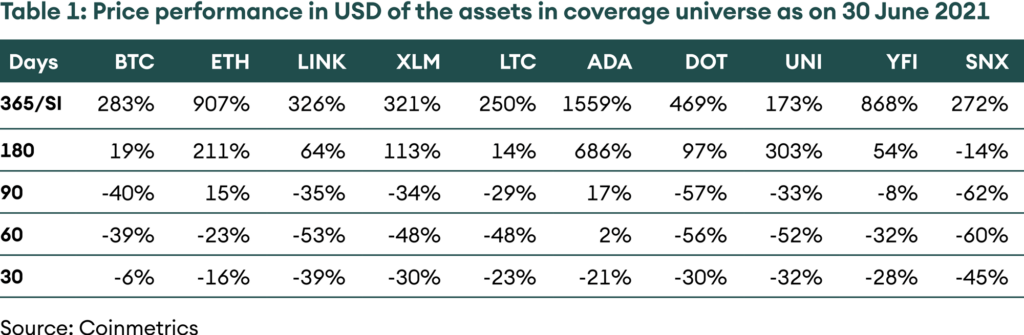

Table 1: Price performance in USD of the assets in coverage universe as on 30 June 2021

The New Digital Investor

Investments in digital assets are becoming increasingly popular and are being used to enhance returns and diversify investors’ portfolios. Crypto investments go beyond Bitcoin as alternative coins or altcoins see increased interest as they provide exposure to upcoming exciting themes.

To cope with the increasing demand, AMINA bank has broadened its offering. Currently, 14 cryptocurrencies and tokens are available. There is Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), Stellar Lumen (XLM), Bitcoin Cash (BCH), Circle’s USD stable coin (USDC), Uniswap (UNI), Synthetix (SNX), Yearn Finance (YFI), Tezos (XTZ), Aave (AAVE), Chainlink (LINK), Polkadot (DOT) and Cardano (ADA).

As digital investment is taking a new dimension, so is our flagship publication: The Digital Investor. As of today, The New Digital Investor succeeds the Digital Investor.

The New Digital Investor is the AMINA Research investment strategy piece. It summarises the Investment Committee house view. It covers the developments of the AMINA coins (more to come!) and their outlook.

Market overview

Since the cryptoasset market peaked in May, all major cryptoassets have taken a hit, and prices have remained under pressure. Measured in US dollar, the proprietary AMINAX® Index dropped by 13.5% in June, more than Bitcoin (-5.3%), illustrating that altcoins have been impacted more heavily.

However, last month’s performance differential should be taken with a pinch of salt. Indeed, the AMINAX® Index year-to-date performance is more than 100%, while price of bitcoin has increased by about 21%, showing the massive outperformance of altcoins so far this year.

The success of altcoins mirrors the rise of DeFi applications that have boomed in the last 12 months. The success of DeFi shows the power of smart contracts and explains why smart contract platforms such as Ethereum, Polkadot and Cardano have also performed strongly.

The question investors are asking is whether the altcoins rally is over or whether it will resume soon.

Bitcoin

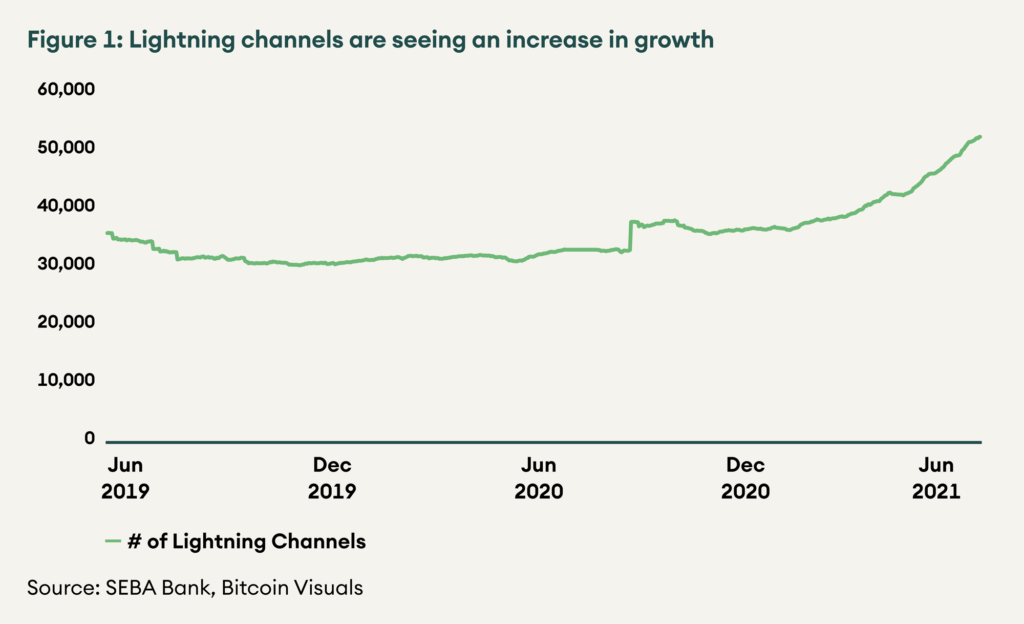

The most positive news for bitcoin for the month was that it was adopted as legal tender in El Salvador. All merchants in El Salvador will accept bitcoin in exchange for the goods and services they provide. To settle day-to-day transactions, Salvadorians will use the lightning network, bitcoin’s scaling solution with much lower fees. This development is exciting for two reasons – first, it will bring a new set of users to the ecosystem and figure 1 shows the increase in adoption of the Lightning network. Secondly, it is important for the precedent it sets – El Salvador is hoping to attract the capital and exceptional talent present in the crypto community. If it is successful in doing so, it may set off a domino effect where other LATAM and developing countries may follow suit.

Figure 1: Lightning channels are seeing an increase in growth

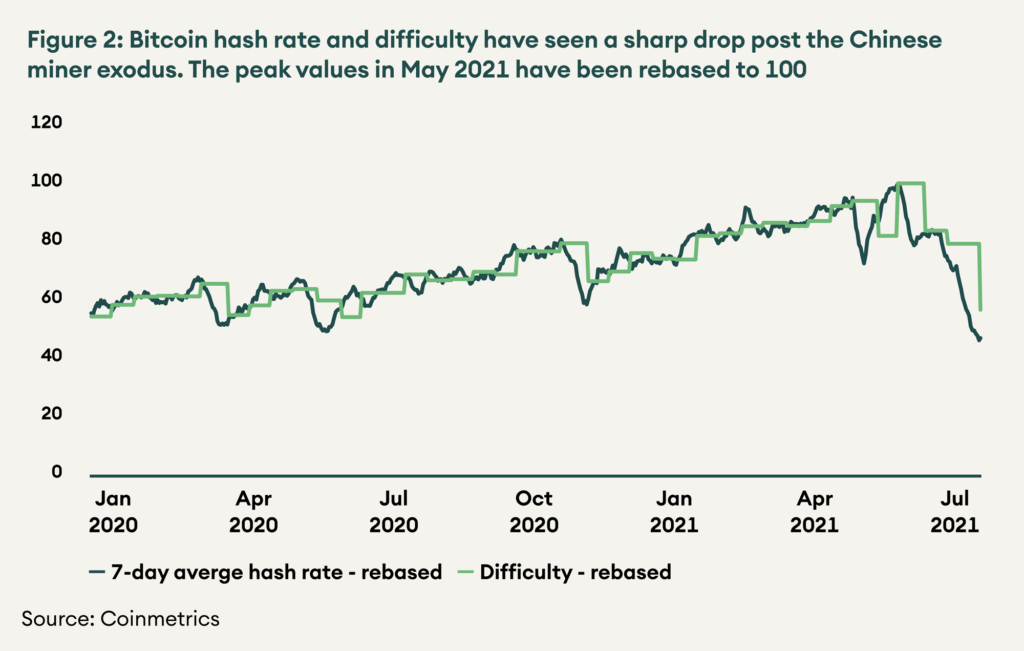

However, regulatory updates were not all positive. Multiple Chinese provinces, including the key mining provinces of Xinjiang and Sichuan, have restricted mining activity in the region leading to an exodus of miners from the country. China controlled more than 65% of bitcoin mining as per a Cambridge report. In the wake of this ban, we expect mining activities to redistribute in the coming months, mainly to Kazakhstan and the US, leading to a renewed increase in hash rate.

Consequently, over the month of June, the bitcoin hash rate halved, leading to average block times of up to 16 mins towards the end of the month. On the 3rd of July, the network experienced its largest difficulty reduction (-28%) on record to bring block times back to the target average of 10 mins. As block times have remained above 10 minutes despite the adjustment, there will be another reduction in difficulty at the next adjustment date, expected around the 19th of July.

The hash rate reduction though widely covered, does not necessarily affect the network significantly negatively. The current network hash rate of 80 exahertz per second is still unrivalled, and the security remains strong as ever. For comparison, the peak hash rate of the Ethereum network is ~650,000 gigahertz per second, i.e., only 0.00065 exahertz per second. This means that it will take >100,000 times more hash power to compromise the Bitcoin network than the Ethereum network.

Figure 2: Bitcoin hash rate and difficulty have seen a sharp drop post the Chinese miner exodus. The peak values in May 2021 have been rebased to 100

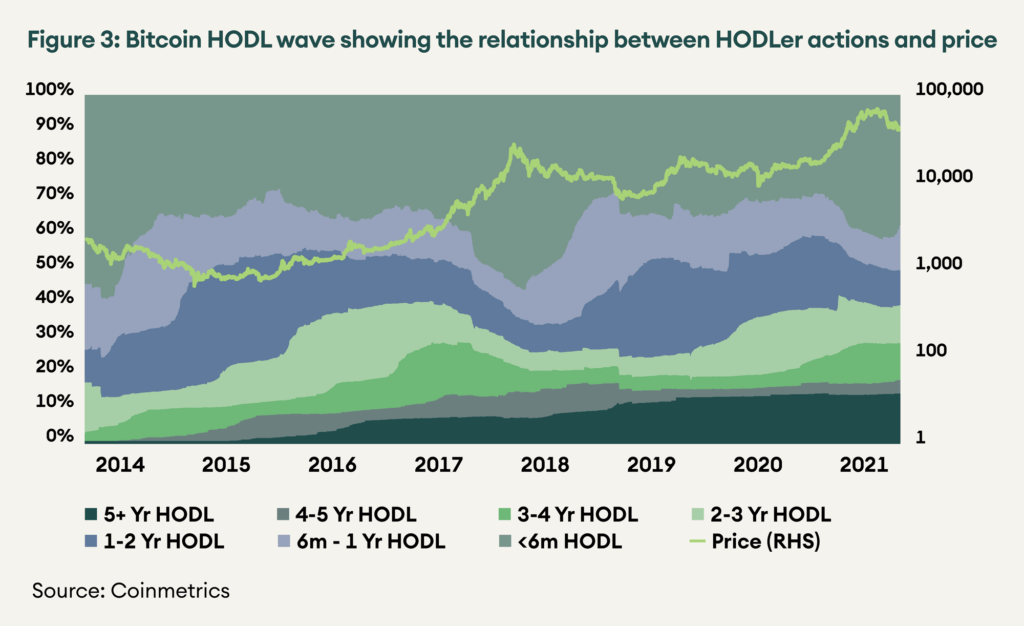

In the second half of last year, bitcoin’s increasing price set off a hype cycle of new adoption and user growth, leading to a further increase in prices. However, with the recent correction, user growth has also stagnated. This effect can be seen in figure 3 by comparing new users (<6m HODL) and the price as both figures increase and decrease in tandem.

Figure 3: Bitcoin HODL wave showing the relationship between HODLer actions and price

It is not easy to estimate all real users as some only use aggregators and exchanges. For example, the peak for bitcoin active addresses is ~1.4 m but Robinhood, in its recent S1 filing, reported that 9.5 m of its users traded crypto assets. Crypto specific exchanges and payment solutions will have even more users. However, if on-chain active addresses are used as a proxy for users, it seems as they have peaked for now. Positive regulatory developments like El Salvador adopting bitcoin as legal tender will be a driver for user growth in the future even if the price-hype-adoption cycle does not return immediately.

Institutional adoption, too, has been a mixed bag. Michael Saylor is betting the house on bitcoin with multiple rounds of debt raised and, more recently, an at-the-money security offering of USD 1 bn. Elon Musk, on the other hand, is flip-flopping from his conviction with Tesla no longer accepting bitcoin in exchange for cars over concerns on the environmental impact of bitcoin mining. Interest and coverage from traditional financial institutions like JP Morgan, Citibank and Goldman Sachs is sustaining currently. It will be interesting to observe whether the institutional adoption trend continues after the recent price action.

Other payment chains – Litecoin and Stellar Lumens

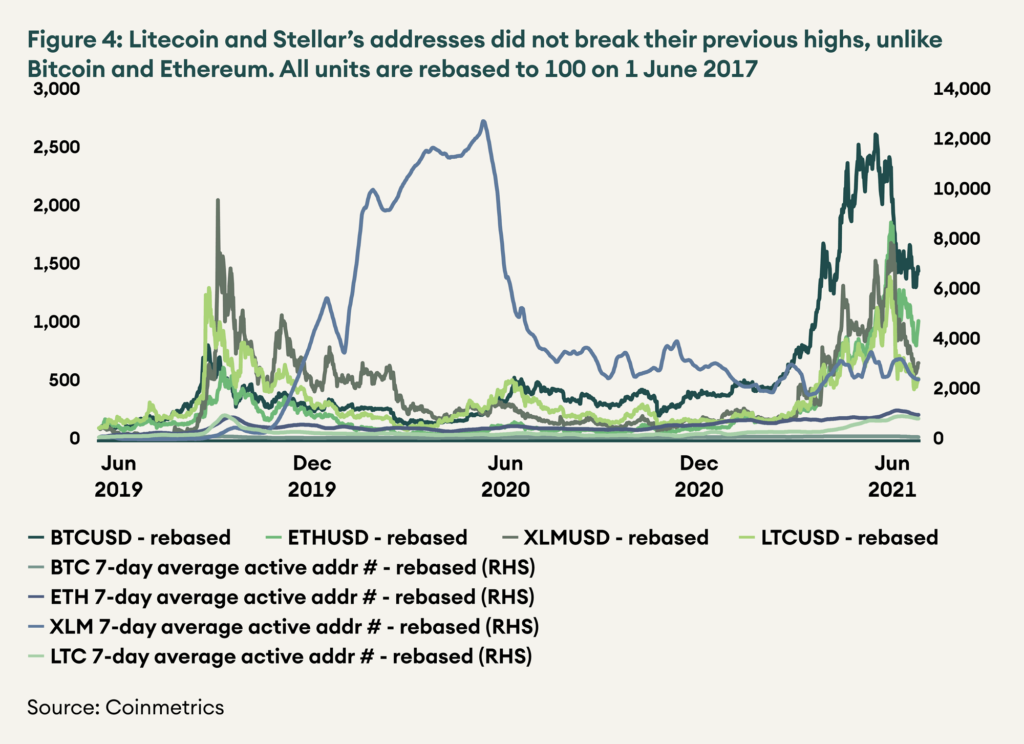

Even though LTC and XLM participated in the bull run, their performances were muted compared to the broader market. BTC and ETH reached new all-time highs about 200% above the previous ones, as did the next-gen coins with new ideas and fresh capital like ADA and DOT. In comparison, LTC’s peak was only 7% higher than its 2018 peak, and XLM has not yet created a new high.

These differences are also reflected in the number of active users. While both Bitcoin and Ethereum chains were able to attract many new users surpassing their previous highs. Litecoin and Stellar have not yet reached their previous peaks of active addresses.

Figure 4: Litecoin and Stellar’s addresses did not break their previous highs, unlike Bitcoin and Ethereum. All units are rebased to 100 on 1-Jun-2017

On 1 January 2020, LTC and XLM were ranked 6 and 11, respectively, by market capitalisation on CoinMarketCap. Today they are ranked 14 and 21, having been eclipsed by platform coins like ADA, DOT and SOL as well as DeFi and infrastructure tokens like UNI, LINK and MATIC. Older generation chains have trouble differentiating themselves in a highly competitive and fast paced environment where interest collects on established projects like BTC and ETH or the new and innovative ones such as DOT and ADA.

Litecoin’s privacy and scaling update, called MimbleWimble, is on track with the lead developer, David Burkett, reporting that he has handed the code over to the reviewing company Quarkslab. The update is slated to be implemented by Q4 2021. Interested readers can read about the improvements MimbleWimble will bring to Litecoin in this linked article by the Litecoin Foundation.

Ethereum

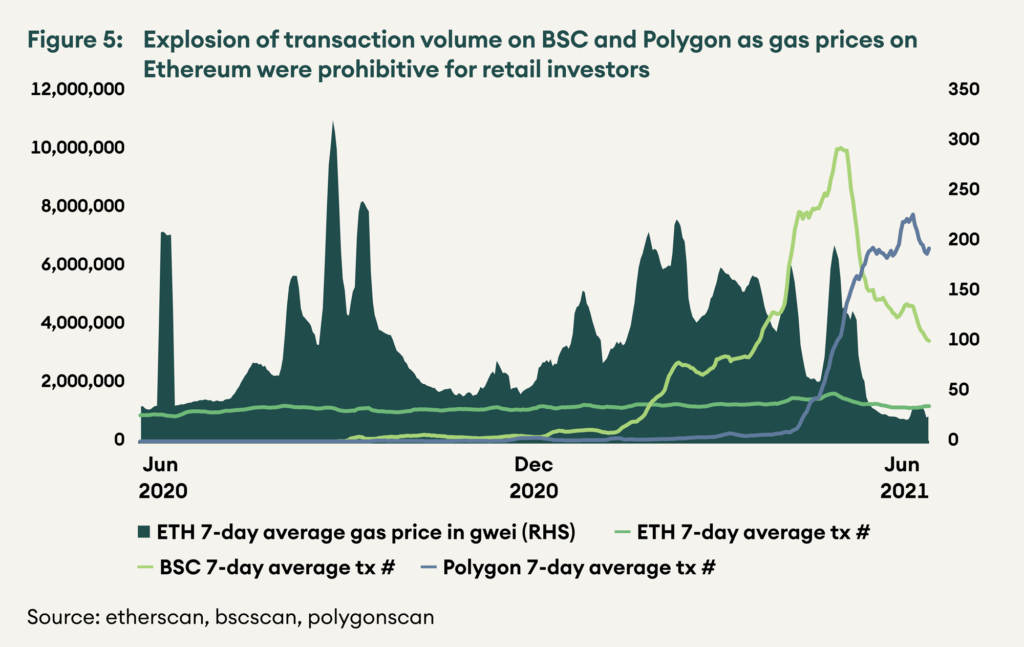

The past 12 months have seen new use-cases like DeFi and NFT being innovated on Ethereum and seeing significant user adoption. Ethereum has suffered from this success, with gas prices remaining elevated for much of Q1 2021 and restricting user growth. As a result, alternatives like Binance Smart Chain (BSC) and Polygon Network (Polygon) have captured market share with a cheaper and faster blockchain. Recently however, BSC and Polygon ecosystems have faced issues of their own. With a low barrier of entry there has been a higher frequency of hacks and pump-and-dump coins. The chains have also faced increased scrutiny and criticism over sacrifices made to decentralisation and security to offer higher scalability. The high degree of activity on these alternate Ethereum Virtual Machine (EVM) chains provides some comfort that if Ethereum can scale, there is latent demand looking for a safer venue to transact.

Figure 5: Explosion of transaction volume on BSC and Polygon as gas prices on Ethereum were prohibitive for retail investors

Ethereum is looking to scale quickly to capture this demand. Arbitrum’s roll up beta went live on the main net in late May, and Optimism’s roll up is expected in July. These solutions are just two of the many teams looking to scale Ethereum and its thriving ecosystem. Others include validium and zero-knowledge roll up solutions by StarkWare, zkSync and more. It will be interesting to see how successful these roll-ups are for Ethereum and, if they are, whether the volumes lost to competing chains will return. The most notable projects on Ethereum like Uniswap, Synthetix and Aave will be supporting one or more of these scaling solutions. We are optimistic that Ethereum’s scaling issues may finally have a solution, at least for the short term, as sharding on Ethereum 2.0 is not expected until the second half of 2022.

Besides the scalability improvements, the Ethereum Improvement Proposal 1559 (EIP 1559) is set to impact ETH in the long term as it rewrites its tokenomics. EIP-1559 allows for greater predictability of gas prices, with all users paying the same BASEFEE for all transactions on a single block. BASEFEE will adjust depending on whether the block is filled more or less than half of its total capacity going up by 12.5% if it is more than 50% full and reducing by the same amount if it is not. To prevent collusion by miners to keep gas fees elevated by artificially filling up blocks, the network will burn this BASEFEE instead of transferring it to the miners. This means that as the network gets used more, there will be a greater amount of ETH that is burnt, reducing the supply. The burning of the BASEFEE aligns the interest of holders, users and developers. EIP-1559 is expected to go live in early August on the main net.

Other platform chains – Cardano and Polkadot

Figure 6: Significant growth in active address and transaction count for ADA and DOT

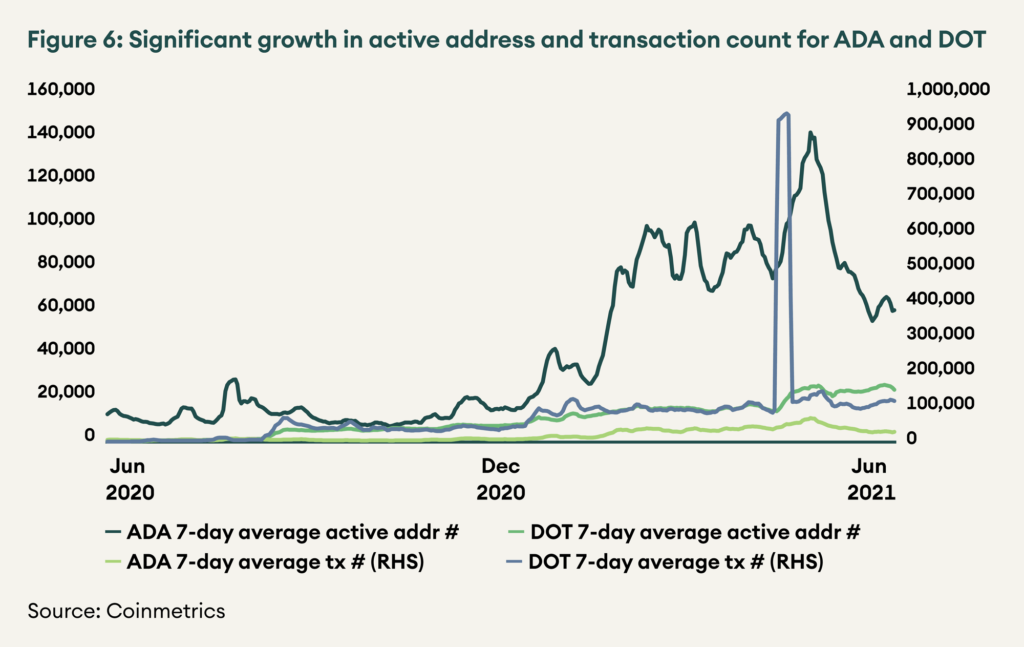

Platform chains have been the primary beneficiaries of this bull run as new use cases like DeFi, interoperability, and NFTs have been adopted by the users. Cardano, in particular, has been an outperformer rising from a market cap rank of 13 in January 2020 to become the fifth-largest project in June 2021 and the largest PoS chain. Polkadot also trades at ~13x of the price at which it last raised funding in July 2020, adjusted for token split.

Cardano’s plan to integrate smart contracts is on track with the first phase of the rollout on the test net, Alonzo Blue, expanding its operator network from 6 to 20. The full rollout is expected to take ~60 more days, with mainnet smart contracts going live in August. Smart contract functionality will allow use cases like DeFi and NFT to work on Cardano. Cardano also had the first-ever token sale on its platform – Revuto raised USD 10 million in ADA. It plans to become a platform that helps manage subscriptions to various services like Spotify and Netflix from a single app and will later integrate with DeFi.

For Polkadot’s future, we look to its Canary Network, Kusama. Kusama parachain auctions are ongoing, with two having concluded successfully at the time of writing. The winner of the first parachain auction was Karura, the DeFi hub for Kusama, as it bonded 500k KSM or about USD 100 mn, and its crowd loan saw participation from >14,000 users. The Polkadot equivalent of Karura is Acala, and if it raises an equivalent amount in terms of market cap (5% of main chain), it will bond USD ~900 mn worth of DOT. The winner of the second parachain auction was Moonriver (Polkadot version – Moonbeam) that bonded 200k KSM. Moonriver is an EVM compatible parachain and will allow developers to bring Ethereum apps to Kusama. A total of 5 Kusama parachains will be auctioned in this run, and Polkadot parachain auctions will follow.

Decentralised Finance

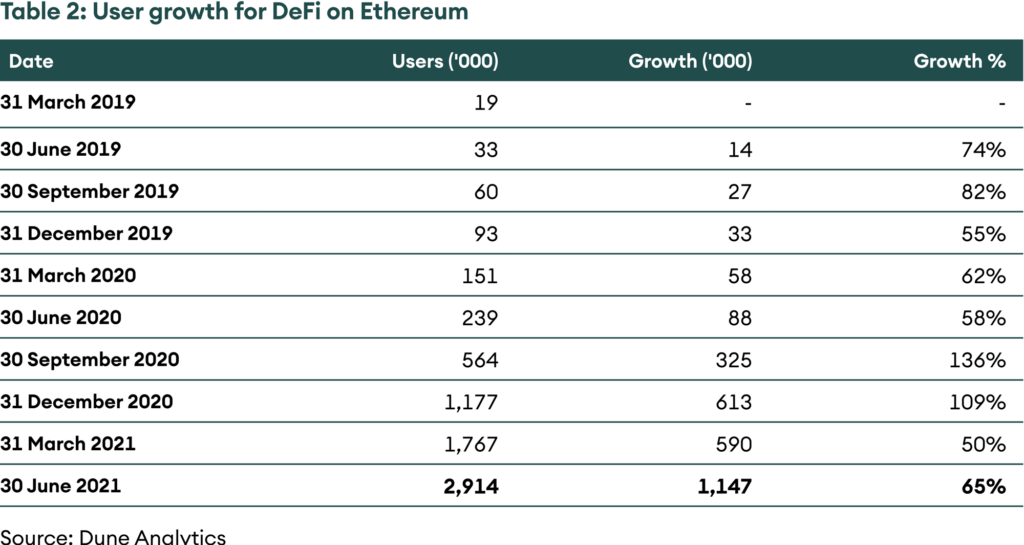

Ethereum based DeFi applications struggled to attract new users as even the absolute number of users added in Q1 2021 was lower than Q4 2020. However, Q2 2021 saw a return of meaningful increase in user growth with over 1 million new users added despite the price correction in the broad crypto assets. High gas fees are deterrent for user growth, now with roll-ups around the corner we expect this growth trend to improve.

Table 2: User growth for DeFi on Ethereum

As centralised finance (CeFi) solutions for crypto assets grow, they increasingly integrate DeFi into their ecosystems. Crypto CeFi now provides integrations with DeFi apps for hassle-free yield farming, liquidity providing, lending and staking. In the medium term, the boundaries between DeFi and CeFi are likely to blur further with a seamless transition, and this will help onboard the next million users.

Uniswap

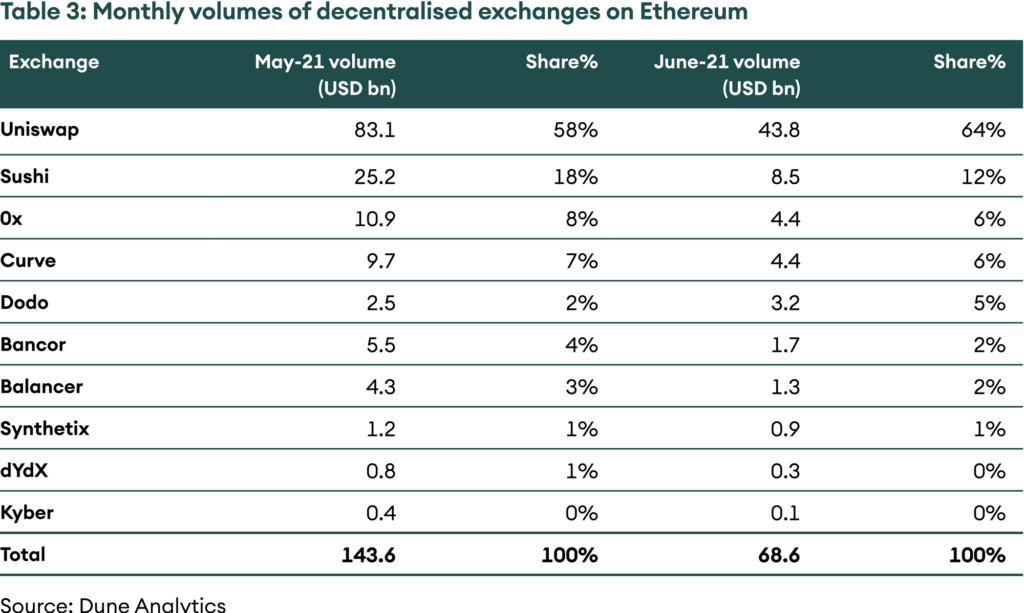

Uniswap exchange is the largest DeFi project by market cap and users. While volumes in June were not as high as in the highly volatile month of May, Uniswap saw an increase in its market share from 58% to 64%. Volumes trended at an average level of USD 1.5 bn with >60% coming from the newly launched v3 AMM. Uniswap benefits when any theme on Ethereum picks up in pace, and there is a noticeable increase in volumes and user activity. This was the case when meme coins like Shiba Inu were trending, for instance. Recently, Coinmarketcap integrated Uniswap’s exchange mechanism on its homepage. Coinmarketcap is one of the most popular crypto asset websites with an Alexa rank of 127, higher than Binance at 138, Coinbase at 549 and Coingecko at 594. Integrations such as these will allow the onboarding of the next leg of users to DeFi, even if it does erode some brand value for Uniswap as the user may not necessarily know or care from which protocol the liquidity is being provided.

Table 3: Monthly volumes of decentralised exchanges on Ethereum

Uniswap has a large governance-controlled treasury of USD 3.5 bn and has attracted the attention of prominent members of the community. Harvard Law School’s Blockchain and Fintech Initiative drafted a proposal for a “DeFi Education Fund” that allocates one million UNI tokens for defending the DeFi space from negative regulation through policymaker education, thought leadership, research and grassroots advocacy. This proposal was passed successfully, garnering support from other prominent delegates such as Blockchain at Columbia University, Penn Blockchain and more. Vitalik Buterin has also proposed that UNI become an oracle token to diversify the reliance on Chainlink, as it also aligns with the current business model of a decentralised exchange.

This sort of active community is an incredible moat for Uniswap and brings to fruition the ideals of blockchain and decentralised governance. As the largest application on any blockchain, it is expected to continue to see active involvement by community members and, with a large treasury, will be in a position to fund the best ideas.

Other DeFi applications

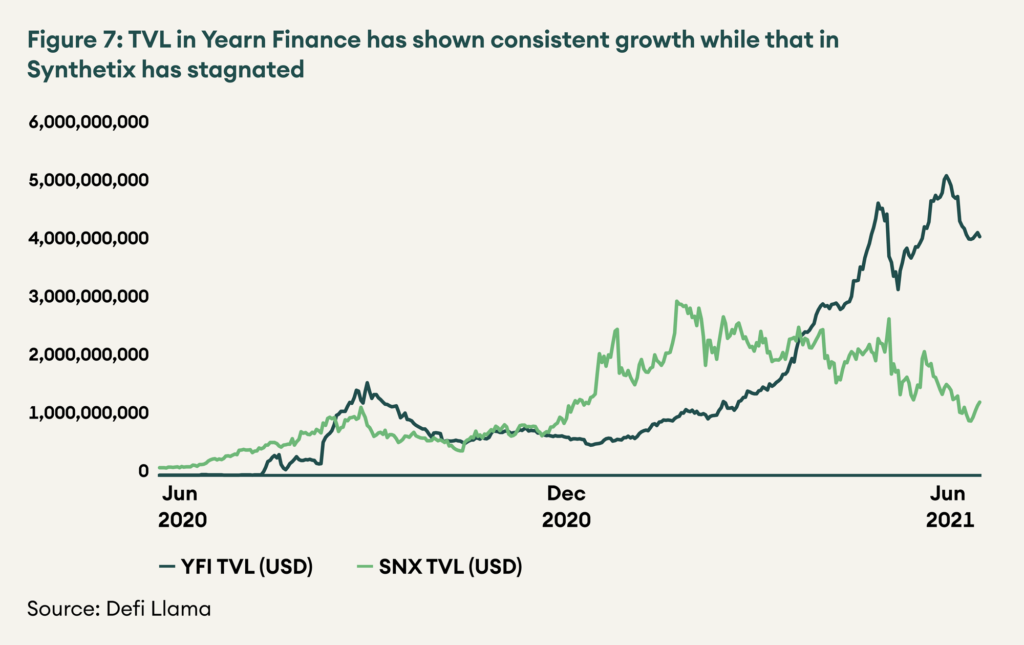

Yearn Finance continues its strong growth in total value locked (TVL) even in a bear market. As exciting opportunities to invest in new coins run dry, passive investing and yield farming through Yearn is likely to seem more lucrative to users. Yearn is able to smartly manage the funds of its 20k users to generate the best possible yields while enjoying economies of scale on transaction costs.

Synthetix has been an underperformer recently, but its poor performance is exaggerated as it had seen a meteoric rise from Q4 2020 to Q1 2021. Synthetix governance had been decentralised with the control being handed over to a decentralised Spartan Council, with the founder Kain Warwick taking a back seat. However, as differences have surfaced among the Core Contributor group, Kain announced his intention to run for Spartan Council to retake a more hands-on approach.

True to the vision of DeFi of small lego blocks building a greater whole, Synthetix is being integrated with other DeFi protocols. Kwenta (previously Synthetix.Exchange) has been spun out, and Lyra and Thales are two ambitious options protocols that use the derivatives and zero-slippage swaps provided by Synthetix protocol.

Figure 7: TVL in Yearn Finance has shown consistent growth while that in Synthetix has stagnated

Chainlink has also been an underperformer recently. Its poor performance is explained by its fast rise before the date of recording. Chainlink was one of the first protocols to participate in the bull run and had risen from a market cap rank of 18 in January 2020 to 5 in August 2020. It is currently ranked 15 and is the second-largest decentralised application. Its use remains ubiquitous across applications, whether DeFi, NFTs or gaming and it is present across chains. Chainlink provides an essential B2B service, and as blockchain adoption and use cases grow, the use of its oracle services will grow. Chainlink has become so dominant and pervasive that it suffers from having become a near-monopoly, and protocols are using other feeds such as Uniswap’s price feed to diversify from this risk.

Conclusion

Crypto assets tend to operate in fast cycles when they become the centre of financial news and developments and see an explosion in price and user activity. As prices have decreased, user and investor interest is also waning. During this cycle, innovative and popular projects surpassed their previous highs in both fundamentals and price. Whenever the hype cycle returns, some of today’s projects will again surpass the highs they have set. In a bear market, fundamentals become even more important and decentralised projects with solid teams and a high degree of community interest are most likely to survive the winter.